Many small business owners considering SBA 7(a) loans worry about the potential costs of early repayment. SBA 7(a) loan prepayment penalties can apply to loans with terms of 15 years or more. This article breaks down the terms, conditions, and eligibility criteria for these penalties. Understanding these details helps businesses make informed financial decisions.

Key Takeaways of SBA 7a Loan Prepayment Penalties

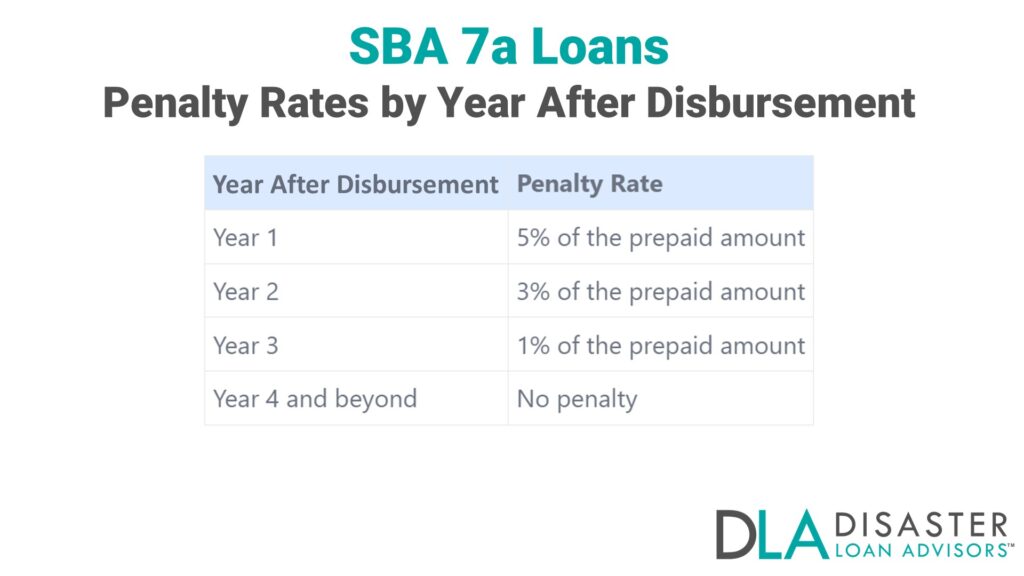

- SBA 7(a) loans over 15 years can have prepayment penalties in the first 3 years.

- Penalties start at 5% in year 1, drop to 3% in year 2, and 1% in year 3.

- Only early payments over 25% of the loan balance trigger penalties.

- Shorter loans under 15 years don’t have these fees.

- Penalties can impact profits and limit options to refinance or sell a business.

Overview of Prepayment Penalties for SBA 7(a) Loans

SBA 7(a) loans often come with prepayment penalties. These fees apply when borrowers pay off their loans early, typically within the first three years.

Penalty rates by year after disbursement

Penalty rates for SBA 7(a) loans vary based on the year after disbursement. These rates encourage borrowers to maintain their loans for the full term while allowing flexibility for early repayment if needed.

Business owners should consider these rates when planning their loan repayment strategy. The penalties decrease over time, offering more flexibility in later years. After the third year, borrowers can repay their loans without incurring any prepayment charges. This structure balances the lender’s need for return on investment with the borrower’s potential need for early repayment. Knowing these terms helps small businesses make informed decisions about their SBA 7(a) loans.

Conditions triggering penalties

SBA 7(a) loan prepayment penalties kick in under specific conditions. These rules protect lenders and ensure borrowers stick to their loan terms.

- Voluntary prepayment: Penalties apply when a borrower chooses to pay off more than 25% of their loan balance early. This rule stops businesses from paying off large chunks of their debt too soon.

- Timing matters: The penalty only affects prepayments made within the first three years after loan disbursement. After this period, borrowers can pay off their loans without extra costs.

- Loan maturity: Only loans with terms of 15 years or longer face these penalties. Shorter-term loans don’t have this restriction.

- Amount threshold: The 25% rule means small extra payments won’t trigger penalties. Borrowers can make minor additional payments without worry.

- Involuntary prepayments: If a lender forces early repayment due to default, the penalty doesn’t apply. It’s only for voluntary actions by the borrower.

- Refinancing limitations: Borrowers who want to refinance their SBA loan within the first three years may face penalties. This rule stops frequent refinancing attempts.

- Partial prepayments: Even paying off just a portion of the loan can trigger penalties if it exceeds the 25% threshold. Borrowers should watch their total prepayment amounts carefully.

- Business sale impact: Selling a business that has an SBA loan might lead to penalties if the sale results in early loan repayment. This affects exit strategies for some business owners.

Eligibility Criteria for Prepayment Penalties

SBA 7(a) loans have specific rules for prepayment penalties. These rules depend on the loan’s term and size.

Loan terms affecting penalty applicability

Loan terms are crucial in SBA 7(a) prepayment penalties. Loans with terms of 15 years or more incur these fees if paid off early. This rule protects lenders from lost interest income on long-term loans. Shorter loans, under 15 years, don’t have these penalties.

Borrowers should consider their payoff plans when selecting loan terms. Longer loans might offer lower monthly payments but come with prepayment risks. Shorter loans avoid penalties but may have higher payments. Disaster Loan Advisors can assist small business owners in evaluating these factors to determine the most suitable option for their needs.

Impact of Prepayment Penalties on Borrowers

Prepayment penalties can hit small business owners hard. These fees cut into profits and limit financial freedom. Business owners may face steep costs if they want to pay off their SBA 7(a) loan early.

The penalties often range from 1% to 5% of the remaining loan balance. This extra expense can strain cash flow and delay growth plans. Some borrowers find themselves stuck with higher interest rates, unable to refinance without incurring hefty fees.

Careful planning helps mitigate the impact of prepayment penalties. Smart borrowers factor these costs into their long-term financial strategies. They weigh the benefits of early payoff against the penalty fees.

In some cases, waiting out the penalty period makes more sense. Other times, paying the fee to secure better loan terms elsewhere proves worthwhile. Each situation calls for a close look at the numbers and business goals.

Frequently Asked Questions About SBA 7a Loan Prepayment Penalties

1. What Are SBA 7(a) Loan Prepayment Penalties?

SBA 7(a) loan prepayment penalties are fees charged when you pay off your small business loan early. These penalties protect lenders from losing interest payments. They apply to loans over 15 years and only in the first three years.

2. How Do Prepayment Penalties Affect My Business Financing?

Prepayment penalties can impact your business financing by adding extra costs if you want to pay off your loan early. This might affect your cash flow and limit your options for refinancing or using working capital for other purposes.

3. Can I Avoid Prepayment Penalties on My SBA 7(a) Loan?

You can avoid prepayment penalties by waiting until after the first three years to pay off your loan. For loans under 15 years, there are no prepayment penalties. Always check your loan agreement for specific terms.

4. Do All SBA Loans Have Prepayment Penalties?

Not all SBA loans have prepayment penalties. SBA 504 loans, for example, don’t have these fees. The rules vary based on loan type, amount, and term. It’s crucial to discuss this with your lender before signing any agreements.

5. How Are Prepayment Penalties Calculated for SBA 7(a) Loans?

For SBA 7(a) loans, prepayment penalties are typically a percentage of the outstanding balance. This percentage decreases each year for the first three years. The exact calculation depends on your specific loan terms and lender policies.

6. Are There Benefits to Paying Off an SBA 7(a) Loan Early Despite Penalties?

Paying off your SBA 7(a) loan early can lead to interest savings and improved cash flow in the long run. However, you need to weigh these benefits against the prepayment penalty. Calculate if the savings outweigh the penalty before deciding.

Conclusion and Summary of Are There SBA 7a Loan Prepayment Penalties?

SBA 7(a) loans offer great chances for small businesses. Yet, owners must grasp the rules on early payoffs. These rules protect lenders and keep loan costs fair. Smart borrowers plan ahead to dodge or lower these fees. They weigh the pros and cons of paying off loans early. Knowing these details helps business owners make wise choices about their loans.

Fuel Your Business Growth with the SBA 7(a) Loan Program: Flexible Funding for Small Businesses!

The SBA 7(a) Loan Program is a versatile financing solution designed to meet the diverse needs of small business owners. Whether you need working capital, funds for expansion, or resources to refinance debt, this program provides the support to help your business thrive.

With the SBA 7(a) Loan Program, you can:

- Access Up to $5 Million for a variety of business purposes.

- Benefit from Competitive Interest Rates and flexible terms.

- Use Funds for Working Capital, Real Estate, Equipment, or Debt Refinancing.

- Enjoy a streamlined application process with support for small business needs.

Eligible Uses for SBA 7(a) Loans:

- Working capital to manage operations and growth.

- Purchasing real estate or long-term leasehold improvements.

- Buying equipment, machinery, or inventory.

- Refinancing existing business debt for better terms.

The SBA 7(a) Loan is tailored to empower small business owners with the flexibility and funding needed to achieve your goals.

Don’t Let Funding Challenges Hold You Back. Take Action Today!Want to discuss if the SBA 7(a) Loan program is right for your business? Schedule Your Free Consultation to see how we can help.

Cover Image Credit: 123RF.com / Lightfieldstudios. Illustration Credit: Disaster Loan Advisors (DLA).

As a leading dedicated member of the Tax and Accounting Team at Disaster Loan Advisors™, Mark focuses on unlocking the ERC Tax Credit's potential for eligible firms that qualify, providing strategic advice, and detailed guidance to ensure substantial financial recovery and growth. His methodical approach to client engagement includes comprehensive deep-dive analysis, customized consultation and guidance, and a commitment to achieving tangible results for each business served.

Disaster Loan Advisors™ (DLA) offers a comprehensive suite of services designed to navigate the complexities of the Employee Retention Tax Credit (ERC) program, ensuring that qualified businesses leverage the maximum possible benefit with minimum hassle. Unlike some firms that charge exorbitant contingency or percentage-based fees (often between 10% to 30% of your ERC refund), DLA operates on a fair and reasonable, transparent flat-fee structure that aligns with the IRS's guidelines.

If you are looking for an ERC Company that believes in providing professional ERC Services and value for small business owners, in exchange for a fair, reasonable, and ethical fee for the amount of work required, Disaster Loan Advisors™ is a good fit for you. STAY SAFE. STAY COMPLIANT. KEEP MORE OF YOUR REFUND.™

- SBA 7a Loans for Healthcare and Medical Businesses - January 26, 2025

- SBA 7a Loans for Non-Profit Organizations - January 25, 2025

- Interest Rate Caps of SBA 7a Loans - January 24, 2025