The Coronavirus Aid, Relief, and Economic Security (CARES) Act introduced the Employee Retention Credit to encourage businesses to keep their staff on the books during the coronavirus pandemic season of 2020.

This tax credit was worth 50% of qualified employee salaries at first, but it was reduced to $10,000 per employee, with a minimum credit of $5,000 for wages received from March 13, 2020, through Dec 31, 2021.

By 2021, the percentage of qualified earnings has increased to 70%. Each employee’s wage maximum has been increased from $10,000 annually to $10,000 per quarter.

The credit is available to all eligible businesses of any size that pay eligible wages to employees; nevertheless, businesses with fewer employees and less than 500 employees must meet additional conditions in various sections of 2020 and 2021.

Key ERC Credit Takeaways You Will Learn:

- Eligibility Requirements for Employee Retention Credit: Understand if your business qualifies for this tax credit to boost your bottom line.

- Qualifying for the Credit: Learn the criteria and steps necessary to ensure your business meets the requirements.

- Not All Employees Are Eligible: Discover which employees are eligible for the Employee Retention Credit and maximize its benefits.

- Meeting Requirements: Familiarize yourself with the specific requirements your business must meet to claim the credit successfully.

- Unlock Your Business’s Potential: Leverage the Employee Retention Credit to claim up to $26,000 per employee and boost your refund.

See Important 2024 Employee Retention Tax Credit Deadline Information at the Bottom of This Article.

What is Employee Retention Credit?

The Employee Retention Credit serves as a transformative measure aimed at repurposing the impact of the Covid-19 pandemic on businesses. It acts as a refundable tax credit intended to incentivize companies to persevere by maintaining employee wages during government-mandated shutdowns.

Determining the Eligibility for Employee Retention Credit

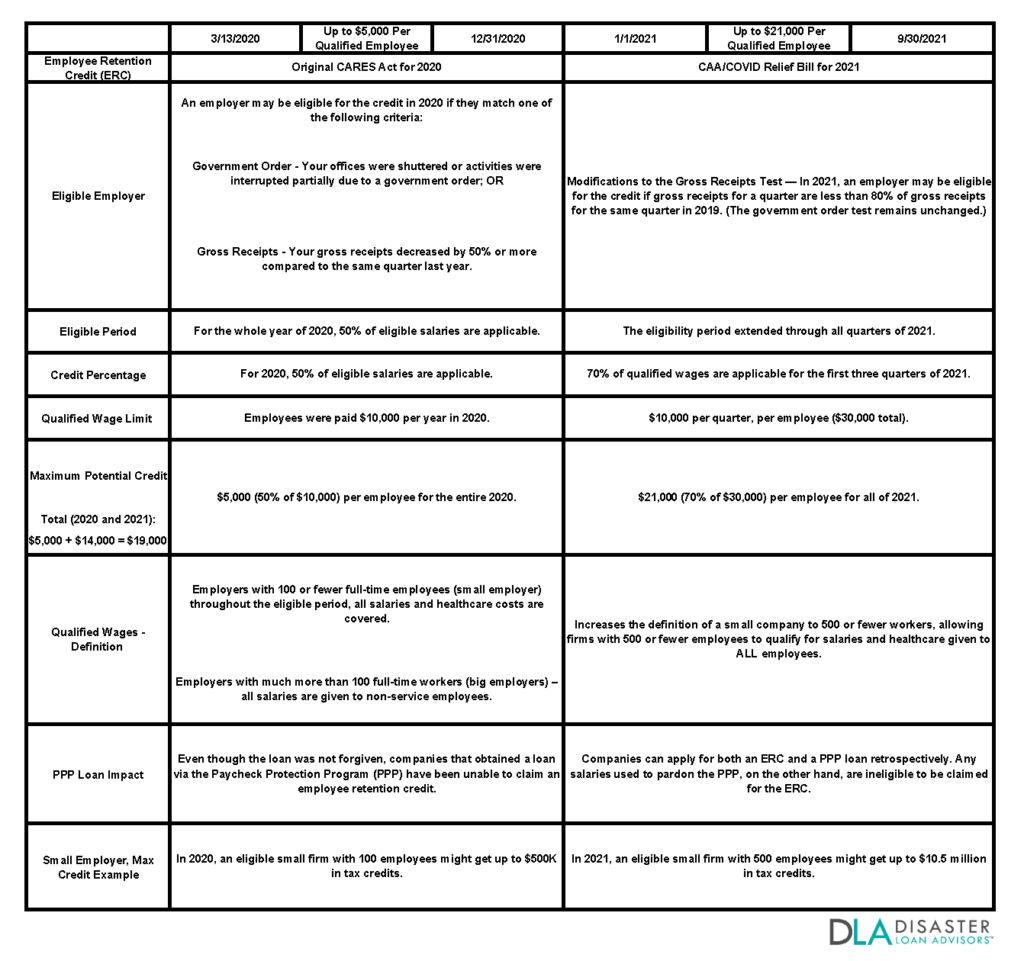

The Coronavirus Aid, Relief, and Economic Security (CARES) Act, which took effect on March 13, 2020, and continues through September 30, 2021, established the Employee Retention Credit (ERC). This may be provided to any company, regardless of the size or employee count, and can also be used in the past.

When operations were at least partially suspended owing to a government order related to the COVID-19 pandemic, the ERC applied to eligible companies(both large and small businesses) that paid qualifying salaries to employees.

The table below lists the key qualifying categories as well as the ERC timelines.

Check out Ultimate Guide to the 2021 Employee Retention Tax Credit (ERTC)

ERC Qualification

As a consequence of the passing of the American Rescue Plan Act, most businesses, including schools, colleges, hospitals, and 501(c)(3) organizations, are now eligible for the credit. The Consolidated Appropriations Act earlier expanded eligibility to include enterprises that took out a PPP loan, as well as borrowers that had previously been ineligible again for the tax credit.

One of two conditions must occur in the calendar month in which the bonus is to be applied for eligible employers:

- Trade was immediately halted or compelled to reduce operation hours due to a governmental edict. The credit is really only valid for the quarter in which the company is closed, not for the entire quarter.

- The Employer’s gross receipts have dropped considerably.

On March 1, 2021, the IRS (Internal Revenue Service) issued Notice 2021-20, which details how businesses may claim the Employees Retention Tax Credit, including how enterprises that got a PPP loan may claim the credit retroactively.

To claim the credit for past quarters, employers must file Form 941-X, Modified Employer’s Quarterly Federal Tax Return or Request in Rebate, for the appropriate quarter(s) in which the qualified wages were paid. The IRS(Internal Revenue Service) gives three examples to show the technique (Q&A No. 57).

The Employee Retention Credit is a tax credit available to the business that desires to keep its employees on the payroll. The credit is 50% of upwards to $10,000 of wages paid by the employer whose business has been entirely or partially shut down as a result of COVID-19 or whose gross sales have reduced by more than 50%.

The benefit is available to employers of any size, especially income organizations. State and local governments, as well as businesses that sign out Small Business Loans, are really the sole alternatives.

The Organization must complete one of two exams in order to be eligible. Each test is computed independently.

Calendar quarter: Either Company’s operations were completely or partially interrupted by government decree due to COVID-19 during the calendar quarter, or the Employer’s total revenues were less than 50% of the equivalent quarter in 2019.

If the Company’s gross revenue surpasses 80% after the end of a similar month in 2019, they are no longer eligible.

Note: The Infrastructure Investment and Jobs Act (IIJA) recently brought about changes to the Employee Retention Credit (ERC). One notable modification introduced by the IIJA is the retroactive exclusion of wages that would have been eligible for the credit in the third and fourth quarters of 2021. However, this exclusion does not apply to a recovery startup business.

Employee Retention Credit Eligibility of the Business

In general, a business qualifies if gross revenue in a fiscal quarter may be less than 50% of the same calendar quarter in 2019. They will no longer be eligible if their quarter’s total revenues hit 80% in the fiscal quarter succeeding the same calendar quarter in 2019.

Firms must have been impacted by forced closures or prevent the spread or have had a 20% drop or significant decline in gross total revenue in the preceding quarter compared to the prior quarter in 2019.

If you’re a new business, it allows you to use gross revenues from your first quarter of business as a reference for any quarterly for which authorities don’t really have 2019 numbers because you’re not yet open for business.

The credit is half of the qualified wages paid, up to a maximum of $10,000. It covers payments made between March 13, 2020, and December 31, 2020. If a company had a little more than 100 employees on average during 2019, the criteria of acceptable pay changes.

Fewer than a hundred The credit is based on salaries provided to all employees, independent of whether they worked if the company has 100 or fewer employees on average in 2019. In other words, even if the employees found a job and were paid for employment, the corporation is given credit.

There are over a hundred. If the company has more than 100 workers on average in 2019, then credit. Only wages paid to employees who did not work during the calendar quarter were allowed.

In both cases, employee wages include not only compensation but also a share of something like the cost of career health care.

Employers can get immediate compensation for refundable payroll tax credit by reducing the amount of payroll taxes collected from employees’ paychecks and submitted to the Government.

Which Business is Eligible for the Employee Retention Credit?

During the calendar year 2020, any private firm or tax-exempt organization engaged in a business profession that:

- Completely or partially halted operations all throughout the calendar quarter in accordance with COVID-19, or Revenue revenues fell considerably during the calendar quarter.

- For 2021, the qualifying standards have been altered.

- To qualify for the credit, more than a tiny portion of the Employer’s company operations must have been discontinued.

For the purposes of employee retention credit, a portion of an employer’s business is considered a negligible significant chunk of processes if either the total revenue from such a component of everyday activities is not less than 10% of its annual gross receipts or the service time performed by the employees here in this sector of the market is just not less than 10% of the total number of hours of work performed by all employees within the company’s business.

Check out Gross Receipts for Employee Retention Credit

Does Employee Retention Credit Apply to Everyone?

Through the Employee Retention Tax Credit program, the government is allowing billions in economic stimulation, yet hundreds of millions of company owners will let most of this money go unclaimed.

Your banks, payroll agency, accountant, legal consultant, bookkeeper, and maybe even your own tax professional have all given you inconsistent advice. Don’t allow gossip and rumor to keep you from getting your refund!

Employee Retention Tax Credits are available to any restaurant that had a full or partial suspension of operations in the previous year, as specified by the occupancy restrictions for indoor eating.

Read full Restaurant ERC tax credit details here.

Business meets across different states follow their respective reopening guidelines, with varying time frames for resuming dining operations. However, businesses are eligible if they faced capacity limitations due to percentage restrictions or if they had to rearrange tables to ensure compliance with social distancing rules.

Learn more about How Does Employee Retention Credit Work.

Qualifying for the Employee Retention Credit

Following the passage of the American Rescue Plan (ARP) Act, most enterprises, especially colleges, universities, clinics, and 501(c)(3) nonprofits, are eligible for the credit. The Annual Finance Act previously expanded eligibility to include businesses that took out loans under the Paycheck Protection Program (PPP), as well as debtors who’ve been previously ineligible for the tax credit.

Note: When an employee qualifies for the Work Opportunity Tax Credit, they cannot be eligible for the employee retention credit for the same period.

One of two conditions must occur in the quarter wherein the benefit is to be applied for eligible businesses:

- A contract was permanently or temporarily suspended or compelled to reduce its hours due to a federal mandate.

- The credit applies only to the period of the quarter wherein the organization was closed, not the entire month.

According to IRS advice, certain firms do not fulfill this factor test and hence do not qualify. Those deemed vital, unless their supply of crucial materials/goods is disrupted in a way that makes it impossible for them to continue operating.

Businesses that were forced to close yet were able to keep their operations mostly intact because of telework. The second-factor test, however, may still qualify any of these enterprises for loans. An employer whose gross earnings have dropped significantly.

The IRS issued a safe harbor (Rev. Proc. 2021-33) on August 10, 2021. It allows companies to exclude PPP loan forgiveness, Forced to shut down Venue Technicians Grant, and Restaurant Revitalization Funds (RRF) from gross receipts when evaluating eligibility for the ERTC. Employers must use this safe harbor consistently across all organizations.

Employee Retention Credit Qualification

The Employee Retention Credit (ERC) Qualification is a refundable employment tax credit equivalent to half of an employer’s employee earnings that may be used for various employment taxes. The program’s goal is to assist firms with the financial resources they need to keep paying their employees.

Employers whose operations were either completely or partially halted as a result of COVID-19 directives or whose gross revenues for any particular quarter in 2020 were below half of those for the same quarter in 2019.

The ERC was already accessible for 2021, with a few adjustments, thanks to the passage of the American Rescue Plan (ARP) Act. This is an important addition to the program since it gives company owners additional opportunities to recover financially.

Since the current financial relief package allows firms to use the Employee Retention Credit (“ERC”) even if they already received Paycheck Protection Program (PPP) cash, it has become the most often asked question.

If an employer is eligible, the maximum credit per worker in 2020 is $5,000, with the credit greatly increasing in 2021 to $14,000 per worker.

For instance, a $250,000 credit ($5,000 x 50 workers), as well as a $700,000 credit ($14,000 x 50 workers), might be achieved in 2020 and 2021, respectively, for a qualifying firm with 50 employees who reach the wage ceiling. These figures can quickly add up to a significant financial impact and should not be overlooked.

The first difference between PPP stimulus financing is that a firm can employ any number of people and yet be an eligible employer for the ERC. The ERC is not limited to small firms; instead, it is open to any qualifying employers that operate a commercial business that fits one of two criteria:

Due to COVID-19 OR directives from an authorized government body restricting commerce, travel, or group meetings, the operation of the trade or company is entirely or partially halted for the calendar quarter.

When compared to quarters from 2019 and 2020, the Employer’s total receipts dropped significantly.

The ERC was not available who were Federal and State organizations or agencies underneath the original CARES Act.

As of Jan 1, 2021, the ERC standards have been amended to allow 501(c)(1) nonprofits that are tax-exempt under section 501(a) and also government companies if the primary purpose or function is to provide medical or hospital treatment, to qualify for the ERC.

How to Qualify for Employee Retention Credit?

For the Employee Retention Tax Credit, eligible firms must report their total qualifying earnings on their federal hiring tax returns, which are usually, Company’s Quarterly Taxation Form, every quarter.

An eligible business can lower its federal employment tax deposit by the qualifying earnings it has already paid from 2020 or 2021. Furthermore, if IRS Form 941 has previously been filed and the ERC is still available, an amended and updated Form 941-X can be submitted to claim the credit.

Such applicable amounts relate to I certain health plan expenses that are treated as eligible wages for (i) ERC purposes, and (ii) wages that the Employer originally chose not to treat as qualifying wages in the hopes of using such wages in determining the business’ PPP debt forgiveness, and for which debt relief does not take place.

Who Qualifies for the Employee Retention Credit?

Employers must be designated “qualified employers” under Internal Revenue Section 52 or 414, based on their business structure, to use the Employees Retention Credit Qualification. Furthermore, for 2020 and 2021, the statute retains various requirements:

A qualifying employer for 2020 is one who can demonstrate one of the following:

That gross receipts for the first quarter of 2020 were less than half of those for the same quarter in 2019.

Alternatively, economic activity may have been halted in part as a result of a government order restricting making deals, traveling, or gathering owing to COVID-19.

A qualified employer for 2021 is one who can prove one of the following:

- That gross revenues for the first quarter of 2021 were less than 80% of those for the same quarter in 2020

- Alternatively, economic activity may have been halted in part as a result of a government order restricting conducting business, traveling, or gathering owing to COVID-19.

- It’s also worth noting that certain firms qualified as a recovery startup business. Only these firms are eligible for an ERC in Q4 2021. Both of the following conditions must be completed to qualify as a Recovery Startup Business:

- After February 15, 2020, the company began operations.

- The company’s gross receipts are less than $1 million.

Note: Employers need to remember that the opportunity for a retroactive refund applies exclusively to the tax year 2020 and the first three quarters of the tax year 2021.

The starting point for qualifying wages paid is the concept of income to use for Social Security and Medicare tax purposes. After that, the wages paid qualify if the following changes are made:

- Only payments made between March 12, 2020, and January 1, 2021, are eligible.

Other restrictions apply, such as the credit being unavailable for salaries for which the Job Opportunity Credit is requested.)

For the purposes of claiming the credit, companies that employed fewer full-time employees(less than 100) on average in 2019 can access the incomes of all eligible workers.

Employers will only be eligible for the credit for qualified wages paid and salaries earned during a period when operations were suspended due to a disease outbreak or a steep reduction in total receipts, and the amount could often exceed what the employee would have earned without the pandemic.

The application of wide aggregation criteria to establish if an employer is large or small for this purpose, such as a greater than 50% ownership rule, might result in parent-subsidiary or buddy relationships.

Internal Revenue Code Section 414(associated)’s service group regulations, as well as Section 414 provisions, apply.

Are All Employees Eligible for Employee Retention Credits?

Qualified earnings, which include specified health plan charges, disbursed throughout any qualifying quarter in which company activities were ceased, qualify for the Employee Retention Credit Qualification.

To grasp this, it’s vital to understand what the law considers a “qualified salary.” Employers can use the Employee Retention Credit Qualification to recover qualified earnings, although the definition of qualified wages varies based on the size of the firm and the number of employees.

If a firm had over 100 workers on average in 2019, eligible earnings include specific healthcare expenditures as well as any payment given to the employees whose services were terminated owing to the company’s financial difficulties.

Employers can recover up to the amount their employee was paid for working a comparable amount of time in the 30 days prior to the time of economic insecurity in this case.

According to what we know so far, if the following requirements are satisfied (during the qualifying quarter), you will most likely be eligible for ERC 2021 update:

Before February 16, 2020, your business was in operation. You either have less than 501 W2 employees in the qualifying quarter, or you are a Severely Distressed Employee.

Either:

A partial or complete government shutdown affected your firm,

AND/OR:

You demonstrate a loss of 20% or more on the Gross Receipts Test for the qualifying quarter.

Even if you have more than 500 part time or full time employees, you may qualify as a Severely Distressed Employer if you suffer a loss of 90% or more.

Utilize the ERC Eligibility and Credit Calculator to see if you passed the Gross Receipts Test.

To see if you’re eligible, use the ERC Eligibility Calculator:

- Calculator for ERC Eligibility

- Make your way to the Calculator.

- At the upper right of your screen, select File > Make a Copy; you now have your own version of the Calculator.

- At the bottom of the spreadsheet, select the appropriate tab:

- If you’re evaluating Q3, go to the tab with that name.

- If you’re evaluating Q4, go to the tab with that name.

- Only modify the numbers in the light grey boxes; do not change the values in the white cells since they include formulae, and changing the formulas will produce mistakes in your calculations.

- The text in the light grey cells is only an example; feel free to remove it and replace it with values that are relevant to your company.

- Examine if you were affected by a government shutdowns in Rows 3–5.

- If you answered yes, go to the ERC Credit Calculation part below; if you answered no, go to the Decline in Gross Receipts section.

To calculate your loss, compare the comparable quarter in 2019 and 2021, and utilize Rows 7–12. You are eligible for ERC if you have a decline in gross receipts by more than 20%. Suppose the drop is more than 90%. Even if you have more than 500 employees, you may qualify as a Severely Distressed Employee and be eligible for credit.

Continue to the ERC Credit Calculation if the answer to Qualified? is Yes; if the response is No, you do not qualify for this quarter.

How Does Your Business Qualify for the Employee Retention Credit?

Businesses of any size are eligible for the credit, and beneficiaries are not required to ask for forgiveness. This isn’t a loan; it’s a credit against your unpaid payroll taxes.

You are Qualified if:

A government agency has ordered your company to close or restrict its hours. During any quarter of 2020 or 2021, your business was completely or partially shut down.

- The credit is only valid for the quarter(s) in which you were affected by the outage.

OR

- Gross receipts for your company have dropped significantly.

- Your gross receipts in any quarter of 2020 were 50% or less than the same period in 2019.

You may choose which quarters to compare. Remember that you’re comparing the first quarter to the first quarter, the second quarter to the second quarter, and so on as the pandemic progresses.

If your company qualifies, up to $10,000 in salaries and health-plan costs for each employee will be increased by 70%. This sum is used to reduce your Social Security taxes liability as an employer. If that amount exceeds what you owe, the difference is a refundable tax credit.

This tax credit is still available for the tax year 2020, but only 50% of the salary and health-plan expenditures given to each employee every impacted quarter is deductible, up to a total of $10,000 for the year.

Do I Qualify for Employee Retention Credit?

A business that is qualified for the employee retention credit may receive the ERC even if the firm has obtained a Small Company Disruption Credit under the paycheck protection program, as per section 206(c) of the Employer Surety & Disaster Tax Reductions Act of 2020.

Any eligible earnings that are not considered payroll expenditures in getting PPP debt forgiveness can be claimed by the eligible company. Any salaries that qualify for the ERC or PPP loan forgiveness program can be allocated to one of these two programs alone, not both.

Please discard the Prudence line of text in the commands for one workforce tax return underneath the line commands for “Non-refundable deposit Component of Employees Retention Credit From Spreadsheet 1,” as the knowledge in that sentence is no longer reliable despite the passing of the Taxpayer Surety or rather Disaster Tax Reductions Act of 2020.

Check out What is the Non-Refundable Portion of Employee Retention Credit

What You Need to Do to Qualify for the Employee Retention Credit?

If you wish to be qualified for the ERC, you must continue your trade or company between 2020 and 2021. The government’s operations may be completely or partially halted.

Review Your Decline in Gross Receipts

Furthermore, your gross receipts decreased in the calendar year compared to the previous year. If all of these factors apply to your small business, you will most likely meet the deadline. The size of your company also factors in this regard. It is critical to get payroll information for your employees from a payroll service.

However, because a spreadsheet or Calculator cannot finish this procedure, you are most certainly missing some information. Furthermore, the ERC has various issues, including documentation of qualifying techniques, collaboration with PPP loans forgiveness, restricted group requirements, and health expenditures.

You must know the number of W-2s issued in 2020 and 2021. These salaries were paid before taxes or after another deduction. Because this employee benefit requires payroll information, you are not eligible if your company does not pay employees with W-2s.

Your small business is qualified for the ERC if it is subject to the federal insurance contribution legislation due to your employee salary structure.

During the pandemic, certain restaurants’ business divisions or locations performed well, while others did not.

Many of these restaurants initially thought they wouldn’t be eligible for the credit, but the criteria to either close down or socially distance indoor dining rooms permitted them to qualify under the partial closure test.

Despite not having a large revenue drop overall, a single-unit idea was able to acquire $300,000 in credits due to government orders over the year.

Gross receipts also include goods that aren’t normally considered gross receipts for financial statement reasons.

Make sure you’re using the correct accounting technique to calculate the reduction of the gross receipts and that you’ve included all things in gross receipts as required by the tax legislation.

Getting Employee Retention Tax Credits

The most recent employee retention credit standards are nearly identical to the IRS’s original requirements. On the other hand, has limited the Qualifying Period to exclude the final quarter of 2021. Special requirements for employers that are significantly financially distressed and part of rescue or recovery startup businesses were also included.

- Companies that made deals in 2020, as well as 2021, are qualified for the ERC, as per the IRS’s guidance if:

- Government directives relating to COVID-19 caused a partial or whole stoppage of commerce or trade.

- This is true if your company took out Paycheck Protection Program (PPP) loans, as provided the ERC salaries aren’t considered payroll expenditures for PPP forgiveness.

- If your firm did not even exist in 2019, the IRS(Internal Revenue Service) could help you determine if COVID-19 laws had enough of an impact on your company to qualify for the ERC.

Also check out more details on How to Claim the Employee Retention Credit (ERC)?

What are the Requirements for the Employee Retention Credit?

Employers must meet the following criteria to be eligible for employee retention credits:

- Cannot have taken out a “forgivable” loan via the Paycheck Protection Program (PPP);

- Nonprofit organizations are qualified for this relief and are exempt from the need for a significant decline in gross income.

- Most employers, excluding governmental employers and self-employed individuals who earn their own income, are eligible for employee retention credits. However, the majority of employers retain the potential to meet the qualifying criteria.

Requirements for Employee Retention Credit

If you want to claim the ERC 2021, make sure you meet the full eligibility criteria and requirements. Working with competent tax planning and advising the company to negotiate the complicated modifications made to the ERC standards is the best method to establish if you fulfill the conditions.

One common misconception that has kept small businesses from applying for the ERC is that they would be denied because their firm has not completely shut down.

Even if your firm did not close, you might still be eligible. You may still be eligible for the credit if your firm shortened hours to facilitate sanitation, restricted the services you offer, or can not access critical equipment due to COVID-19.

Many company owners also assume they are ineligible for the ERC if their income has not dropped by 50% or if their company has expanded in the previous year.

Furthermore, popular ERC fallacies like “I can’t claim ERCs since I have greater than 500 employees” or “I can’t claim ERCs since my firm never shut down” inhibit business owners from determining if they qualify.

Many tax professionals are familiar with the ERC program’s complexities as well as the IRS’s numerous adjustments. If your company qualifies, they will make sure you get the most credit possible based on your financial facts.

Are All Employees Eligible for the Employee Retention Credit?

If a corporation (or a charitable organization classified under 501(c) of the Internal Revenue Code and free against tax by 501(A)) is:

- During the calendar quarter, fully or partially halted by a decree issued owing to COVID-19; or

- The Company’s gross revenue was less than 50% of the comparable period in 2020 (once gross revenue exceeded 80% of a similar quarter in 2019, the Employer no longer qualifies at the conclusion of such quarter);

- Needs to continue to compensate its employees

As a result, each employee can receive up to $5,000 from the national govt each of the qualifying quarters listed above.

Check out Employee Retention Credits – A Detailed FAQ Guide.

Do All Employees Meet Eligibility for the Employee Retention Credit?

If the company or a charitable organization is:

- During the calendar quarter, COVID-19 was wholly or partially halted by government order; or

- The Employer’s gross receipts are less than 80% of the corresponding quarter* in 2019 (20% decrease in sales) (after the Employer’s gross receipts are more than 80% of a similar quarter in 2019, they no longer be eligible after the conclusion of that quarter);

- And pays its employees.

There is a safe harbor that permits companies to calculate eligibility based on past quarter gross receipts. If you don’t qualify in Q1 2021, for example, you can compare revenues from Q4 2020 to Q4 2019.

You are not locked in after using this approach; you can opt to employ the “2019 vs. 2021” strategy for the next quarter. Each employee’s eligible pay must not exceed $10,000 each quarter. So, for each employee throughout each quarter listed above, you may get up to $7,500 back from the federal government.

Which Business Industries Are Qualified for the Employee Retention Credit?

Eligible industries for Employee Retention Credit (ERC) benefits include:

- Not-For-Profit

- Industrial

- Law firms and attorneys. (Check ERC guide for law firms and attorneys.)

- Technology, Media, and Telecommunications

- Professional Services

- Healthcare and Life Sciences

- Government Contractors

- Education

- Transportation and Logistics

- Hospitality and Retail

- Real Estate and Construction

What is the Time Frame Required for the IRS to Issue a Refund After Submitting an Amended Form 941X?

IRS refund processing time for amended Form 941X varies (around 5 to 9 months). Factors affecting refund include form volume, tax law changes, and claim filing time. Stay updated and file promptly.

Note: In the past, employers meeting the criteria, with fewer than 500 full-time employees, would have been able to seek advance payment of the ERTC by utilizing IRS Form 7200. While large employers surpassing the 500-employee mark are ineligible to receive an advanceable ERTC. Form 7200 is no longer used, nor can advance payments be received anymore. Only Form 941-X can be used to claim the ERC Tax Credit.

What Is the Due Date to Submit an Application For ERC?

Despite the expired tax credit, eligible employers can still claim qualified wages until December 2023 for the period and benefit until April 15, 2024.

Conclusion and Summary on Determining Your Eligibility for the Employee Retention Tax Credit (ERTC)

If your company’s gross income was disrupted or decreased in 2020 or 2021 compared to 2019, you might be qualified for the Employee Retention Credit (ERC). The ERC was put in place to encourage firms to keep people on the payroll throughout the pandemic.

Recent ERC qualifying and extension adjustments have made the credit more accessible to more enterprises. Find out more about ERC and how to see whether your company qualifies for this IRS incentive. Obtaining the ERC can help your firm and give financial relief from COVID-19-related expenses.

IMPORTANT: The content contained in this ERC Tax Credit Guide serves as a general resource and should not be interpreted as legal, accounting, or tax advice. It’s best to consult with a professional like Disaster Loan Advisors for guidance before filing to take advantage of the maximum tax credit your business can legitimately claim per IRS rules and guidelines.

Read: Avoid Employee Retention Credit Scams: Protect Your Business

ERC PDF Download of This News Article

Download a PDF version of How to Determine Eligibility for the Employee Retention Credit (ERC)?

Employee Retention Tax Credit (ERC / ERTC) Help: Claim Up To a $26,000 Refund Per Employee for Your Business

Disaster Loan Advisors can assist your business with the complex and confusing Employee Retention Credit (ERC) and Employee Retention Tax Credit (ERTC) program.

Depending on eligibility, business owners and companies can receive a maximum ERC of up to $26,000 per employee based on the number of W2 employees you had on the payroll in 2020 and 2021.

The ERC / ERTC Program is a valuable tax credit you can claim. This is money you have already paid to the IRS for payroll costs associated with your W2 employees.

Schedule Your Free Employee Retention Credit Consultation to ask questions about ERC and see what amount of employee retention tax credit your company qualifies for.

ERC Deadline Urgency in 2024

April 15, 2024 Deadline for the 2020 ERC Tax Year

The deadline is coming up for the final opportunity to retroactively claim your business Employee Retention Credit for the past 2020 tax year. With the April 15, 2024 deadline fast approaching, we urge you; don’t let this final chance pass!

While not all businesses will qualify, as it depends on multiple factors per IRS Rules and Guidelines, you might be leaving significant financial relief on the table from past COVID harm to your business during the past 2020 and 2021 business operation years.

Last year, in September 2023, the IRS temporarily paused processing ERC Claims for the remainder of last year. We at Disaster Loan Advisors (DLA) predicted this over one year ago when we made this ERC video warning business owners. See the ten-minute mark of the video for details.

TAKE ACTION NOW IN 2024

Even though the IRS had temporarily paused processing, you will still want to check eligibility and file now (if you qualify) because the IRS will resume processing tax credit claims in the order they are received.

If you haven’t previously filed for the ERC Credit, it is worth scheduling a phone call to at least explore your possible eligibility from both the past 2020 and 2021 business tax years. Contact us today for a deep-dive analysis to determine if your business qualifies one or more quarters from 2020 and / or 2021 tax years.

Cover Image Credit: 123RF.com / Pressmaster. Illustration by: Disaster Loan Advisors.

As a leading dedicated member of the Tax and Accounting Team at Disaster Loan Advisors™, Mark focuses on unlocking the ERC Tax Credit's potential for eligible firms that qualify, providing strategic advice, and detailed guidance to ensure substantial financial recovery and growth. His methodical approach to client engagement includes comprehensive deep-dive analysis, customized consultation and guidance, and a commitment to achieving tangible results for each business served.

Disaster Loan Advisors™ (DLA) offers a comprehensive suite of services designed to navigate the complexities of the Employee Retention Tax Credit (ERC) program, ensuring that qualified businesses leverage the maximum possible benefit with minimum hassle. Unlike some firms that charge exorbitant contingency or percentage-based fees (often between 10% to 30% of your ERC refund), DLA operates on a fair and reasonable, transparent flat-fee structure that aligns with the IRS's guidelines.

If you are looking for an ERC Company that believes in providing professional ERC Services and value for small business owners, in exchange for a fair, reasonable, and ethical fee for the amount of work required, Disaster Loan Advisors™ is a good fit for you. STAY SAFE. STAY COMPLIANT. KEEP MORE OF YOUR REFUND.™

- SBA 7a Loans for Healthcare and Medical Businesses - January 26, 2025

- SBA 7a Loans for Non-Profit Organizations - January 25, 2025

- Interest Rate Caps of SBA 7a Loans - January 24, 2025