The “Nonrefundable Portion of Credit for Qualified Sick and Family Leave Wages” section is listed as question #17 under Part 3 of Form 941-X, which is needed to claim the employee retention tax credit. Instructions are below for the Nonrefundable Portion of Credit for Qualified Sick and Family Leave Wages section.

Key 941-X Tax Form Takeaways:

- Understanding Nonrefundable Credits: Grasp the concept of nonrefundable tax credits, which can only offset taxes owed and are not paid back if they exceed the tax liability.

- Correcting Form 941 Errors: Learn how to properly amend errors related to the non refundable portion of sick and family leave wages on Form 941-X, including the specific steps to calculate and report adjustments.

- Specificity in Reporting: Recognize the importance of accurately reporting qualified sick and family leave wages that meet specific legislative criteria to ensure correct credit calculations.

See Important 2024 Employee Retention Tax Credit Deadline Information at the Bottom of This Article.

Form 941-X:

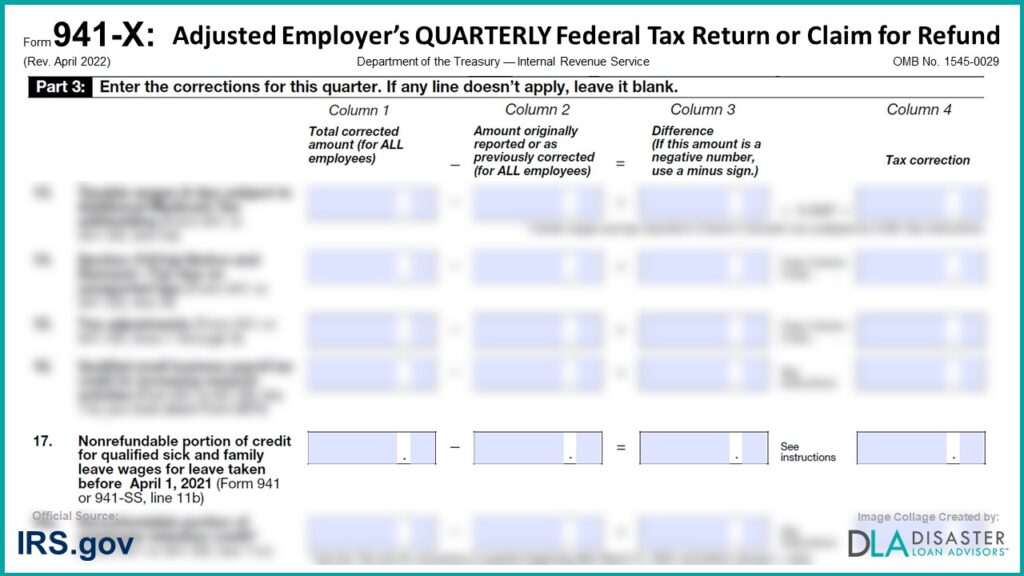

17. Nonrefundable Portion of Credit for Qualified Sick and Family Leave Wages

Part 3: Enter the corrections for this quarter. If any line doesn’t apply, leave it blank.

17. Nonrefundable portion of credit for qualified sick and family leave wages for leave taken before April 1, 2021 (Form 941 or 941-SS, line 11b)

Adjusted Employer’s QUARTERLY Federal Tax Return or Claim for Refund

Part 3, “17. Nonrefundable Portion of Credit for Qualified Sick and Family Leave Wages“ from Form 941X published by the Department of the Treasury – Internal Revenue Service (IRS), OMB No. 1545-0029, revised in April 2022.

Instructions for Form 941-X:

17. Nonrefundable Portion of Credit for Qualified Sick and Family Leave Wages

TIP: Form 941-X and these instructions use the terms “nonrefundable” and “refundable” when discussing credits. The term “nonrefundable” means the portion of the credit which is limited by law to certain taxes. The term “refundable” means the portion of the credit which is in excess of those taxes.

If you’re correcting the nonrefundable portion of the credit for qualified sick and family leave wages for leave taken after March 31, 2020, and before April 1, 2021, that you reported on Form 941, line 11b, enter the total corrected amount from Worksheet 1, Step 2, line 2j, in column 1. In column 2, enter the amount you originally reported or as previously corrected. In column 3, enter the difference between columns 1 and 2. For more information about the credit for qualified sick and family leave wages, go to IRS.gov/PLC.

Copy the amount in column 3 to column 4. However, to properly show the amount as a credit or balance due item, enter a positive number in column 3 as a negative number in column 4 or a negative number in column 3 as a positive number in column 4.

Definition of qualified sick and family leave wages for leave taken after March 31, 2020, and before April 1, 2021. For purposes of the credit for qualified sick and family leave wages, qualified sick and family leave wages are wages for social security and Medicare tax purposes, determined without regard to the exclusions from the definition of employment under sections 3121(b)(1)–(22), that an employer pays that otherwise meet the requirements of the Emergency Paid Sick Leave Act (EPSLA) or the Emergency Family and Medical Leave Expansion Act (Expanded FMLA), as enacted under the FFCRA and amended by the COVID-related Tax Relief Act of 2020. However, don’t include any wages otherwise excluded under sections 3121(b)(1)–(22) when reporting qualified sick and family leave wages on your employment tax return and when figuring the credit on Worksheet 1, Step 2, lines 2a and 2a(i), and on Step 2, lines 2e and 2e(i). Instead, include qualified sick leave wages and qualified family leave wages excluded from the definition of employment under sections 3121(b)(1)–(22) separately in Step 2, line 2a(iii) and/or line 2e(iii), respectively, before you figure your total credit in Step 2, line 2d (credit for qualified sick leave wages), or Step 2, line 2h (credit for qualified family leave wages).

The April 2020 revision and July 2020 revision of the Instructions for Form 941 were released before the COVID-related Tax Relief Act of 2020 was enacted on December 27, 2020; therefore, Worksheet 1, in those Instructions for Form 941, didn’t include lines to add the wages that meet an exclusion under sections 3121(b)(1)– (22) when figuring the credits for qualified sick and family leave wages. If your Form 941 for the second, third, or fourth quarter of 2020 didn’t claim the correct amount of the credit for qualified sick and family leave wages because you paid qualified sick leave wages and/or qualified family leave wages that meet an exclusion under sections 3121(b)(1)–(22), you may file Form 941-X and complete Worksheet 1 to claim the correct amount of the credit. You’ll also include on Form 941-X, lines 28 and 29, and on Worksheet 1 any qualified health plan expenses allocable to those wages. The appropriate lines related to the exclusions under sections 3121(b)(1)–(22) were added to Worksheet 1 in the first quarter 2021 Instructions for Form 941 (Revised March 2021).

Example – Nonrefundable portion of credit for qualified sick and family leave wages increased. Following Example—Qualified sick leave wages increased in the instructions for line 9, you originally reported a $1,000 nonrefundable portion of the credit for qualified sick and family leave wages on Form 941, line 11b, for the second quarter of 2020. You use Worksheet 1 to refigure the correct nonrefundable portion of the credit for qualified sick and family leave wages and you determine that the correct credit is now $2,000. To correct the error, figure the difference on Form 941‐X as shown.

To properly show the credit increase as a reduction to your tax balance, enter the positive number in column 3 as a negative number in column 4. Here is how you would enter the numbers on Form 941‐X, line 17.

Be sure to explain the reasons for this correction on line 43.

Adjusted Employer’s QUARTERLY Federal Tax Return or Claim for Refund

Instructions for Part 3, “17. Nonrefundable Portion of Credit for Qualified Sick and Family Leave Wages“ came from the IRS Instructions for Form 941-X published by the Internal Revenue Service (IRS) Department of the Treasury, revised in April 2022.

Conclusion and Summary on 941-X: 17. Nonrefundable Portion of Credit for Qualified Sick and Family Leave Wages, Form Instructions

The “Nonrefundable Portion of Credit for Qualified Sick and Family Leave Wages” section is just one of forty three detailed questions and calculations you must complete correctly on the 941X IRS Form. Listed as question #17 under Part 3 of the 941X, be sure to answer the Nonrefundable Portion of Credit for Qualified Sick and Family Leave Wages question #17 correctly.

How To Fill Out Form 941-X For the Employee Retention Tax Credit?

Need Help Completing / Filing IRS Form 941-X?

Disaster Loan Advisors can assist your business in filing an amended Form 941 Employer’s Quarterly Federal Tax Return (for 2020 and 2021), which is IRS Form 941-X Adjusted Employer’s Quarterly Federal Tax Return or Claim for Refund.

This tax form is required to be filled out correctly and filed for each qualifying quarter in 2020 and 2021 to ensure your business claims the maximum Employee Retention Credit (ERC) / Employee Retention Tax Credit (ERTC).

– Did you calculate your company’s maximum ERC Tax Credit correctly?

– Are you claiming all the ERC Credit for each qualifying quarter?

– Are you maximizing the total amount of ERC Credit your company qualifies for?

– Need a professional set of eyes to ensure you filled out your form 941X correctly?

Flexible and Professional ERC Consulting Tax Services

There are several flexible options for you. We can review, prepare, and / or file your 941-X Forms for you, or with you.

– Do-It-Yourself (DIY) and have us review your work.

– Done-With-You (DWY) and let’s collaborate together.

– Done-For-You (DFY) and we handle it all for you, from start to finish.

– Or, Consult-With-You to customize to your exact needs.

Our professional ERC fee and pricing structure is very reasonable in comparison.

We DO NOT charge a percentage (%) of your ERC Refund like some companies are charging. Some ERC firms out there are charging upwards of 25% to 35% of your ERC refund!

If you are looking for an ERC Company that believes in providing professional ERC Tax Services and value for small business owners, in exchange for a fair, reasonable, and ethical flat-fee for the amount of work required, Disaster Loan Advisors is a good fit for you.

Form 941-X and the ERC program can be very confusing as it relates to your specific business situation. Our fee structure is fair and reasonable for the same or better level of ERC service.

Schedule Your Form 941-X Consultation to have peace of mind you are making sure your company actually qualifies, AND you are calculating the employee retention tax credit properly.

Deadlines to File IRS Form 941-X in 2024 and 2025

The 2020 ERC Credit Tax Year deadline of 4/15/24 has already passed. Good news? The opportunity to retroactively claim your business Employee Retention Credit for the prior 2021 Tax Year is still available, with a next year April 15, 2025 deadline.

This really is your FINAL chance at any potential ERC tax credit refund!

How to Claim the Employee Retention Tax Credit (ERC / ERTC) and Receive Up to a $26,000 Refund Per Employee

Disaster Loan Advisors can assist your business with the complex and confusing Employee Retention Credit (ERC) and Employee Retention Tax Credit (ERTC) program.

Depending on eligibility, business owners and companies can receive up to $26,000 per employee based on the number of W2 employees you had on the payroll in 2020 and 2021.

The ERC / ERTC Program is a valuable tax credit you can claim. This is money you have already paid to the IRS in payroll taxes for your W2 employees.

Schedule Your Free Employee Retention Credit Consultation to see if your company qualifies for the employee retention tax credit.

Cover Image Credit: Irs.gov / Form 941-X / Disaster Loan Advisors.

As a leading dedicated member of the Tax and Accounting Team at Disaster Loan Advisors™, Mark focuses on unlocking the ERC Tax Credit's potential for eligible firms that qualify, providing strategic advice, and detailed guidance to ensure substantial financial recovery and growth. His methodical approach to client engagement includes comprehensive deep-dive analysis, customized consultation and guidance, and a commitment to achieving tangible results for each business served.

Disaster Loan Advisors™ (DLA) offers a comprehensive suite of services designed to navigate the complexities of the Employee Retention Tax Credit (ERC) program, ensuring that qualified businesses leverage the maximum possible benefit with minimum hassle. Unlike some firms that charge exorbitant contingency or percentage-based fees (often between 10% to 30% of your ERC refund), DLA operates on a fair and reasonable, transparent flat-fee structure that aligns with the IRS's guidelines.

If you are looking for an ERC Company that believes in providing professional ERC Services and value for small business owners, in exchange for a fair, reasonable, and ethical fee for the amount of work required, Disaster Loan Advisors™ is a good fit for you. STAY SAFE. STAY COMPLIANT. KEEP MORE OF YOUR REFUND.™